April 2021 may be remembered by some as the month in which at least part of the air cargo figures returned to some kind of normality. Although worldwide volumes were up by 53% and wide-body capacity by a ‘matching’ 51% year-over-year (“YoY”), air cargo increased by a much more ‘normal’ 3% when compared to April 2019. Yet, it is not unjustified to speak of a business continuing to be turned upside down, as many other measures were not even near ‘normal’.

The average rate/kg went up from an already ‘unheard of’ level of USD 3.12 in March to USD 3.30, even though it came down by 12% from the crazy level of April 2020. Wide-body freighter capacity increased by 1% YoY, but what to think of the changing role of w/b passenger aircraft? They produced one-fifth of total cargo capacity in April 2020, when many passenger flights were cancelled. A year later, the figures are completely different: in April 2021, cargo capacity on w/b passenger aircraft almost tripled YoY, and comes very close to the total capacity produced on w/b freighters.

Although the question by definition cannot be answered, many people would like to find out what would have happened without COVID. Trying to make any sense of air cargo developments, calls for comparing this year with the pre-COVID-year of 2019., which leads to the following overview for the month of April:

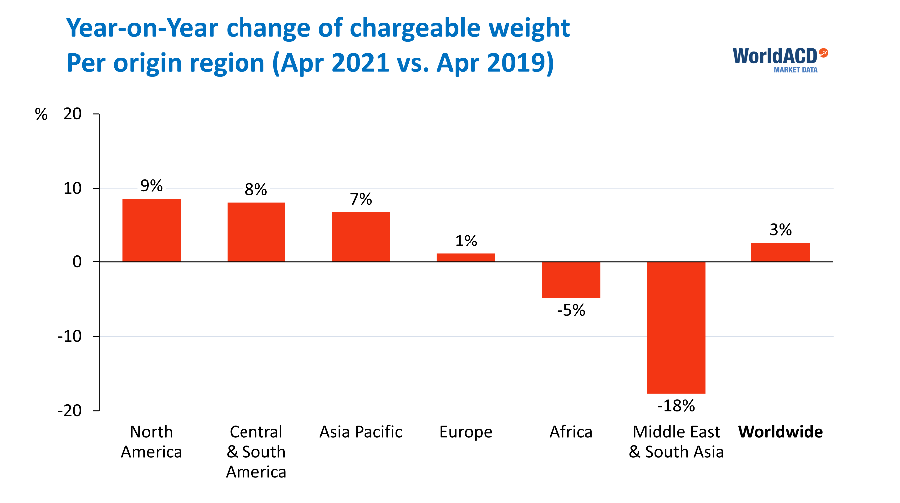

The Americas actually gained most in air cargo exports (+8%), a bit more than Asia Pacific (+7%) and Europe (+1%). Africa (-5%) and the Middle East & South Asia (MESA, -17%) were less fortunate. One level lower, we see Mexico (+14%), North East Asia (+12%) and USA (+10%) as clear winners, whilst Australasia (-27%), the Gulf Area (-22%), South Asia (-19%) and Southern Africa (-17%) show seriously weakened positions.

Continuing this “Yo2Y”- comparison, the growth of Express business has been most impressive (+59%), shipments in excess of 5,000 kilograms increased by 32%, reflecting the growing importance of charters during the COVID-period. All other so-called ‘weight breaks’ showed a volume decline. Rates are still 83% up worldwide, but continue to show very large regional differences: from Asia Pacific they have more than doubled (+117%), but from the Americas and Africa they increased by 30% ‘only’. Judging by some daily news messages, one would think that the rate increases from China to Europe (+117%) and to North America (+152%) are in a class of their own. Yet, this view completely overlooks the fact that rate increases from Europe to North America were 137%... A look at the 20 largest country-to-country markets, shows that rates in markets other than those originating in Asia Pacific, more than doubled from Germany to USA Midwest and from Germany to USA Atlantic South. In the other Top-20 markets, rate increases were comparatively modest.

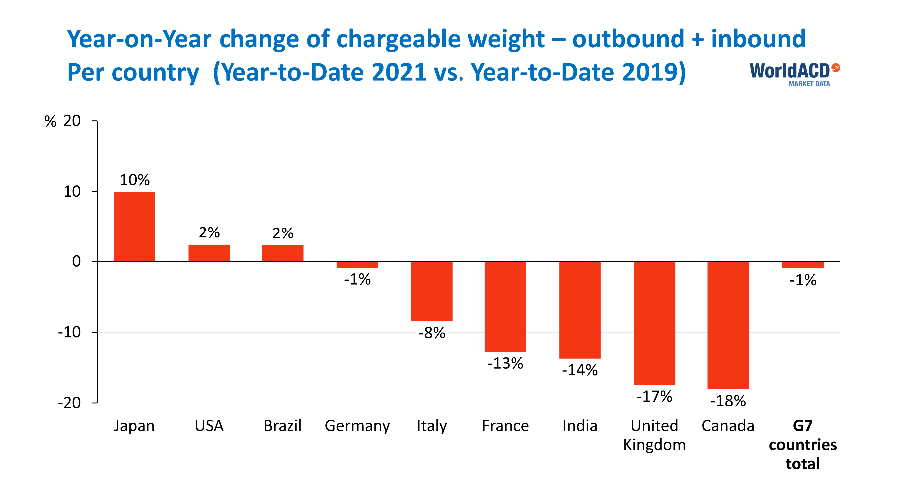

Did the world’s largest economies outside China weather the COVID-storm? We looked at the overall air cargo performance (export + import) in the first 4 months of 2021 compared to 2019. India lost 14% in volume, the group of G7-countries lost 1%, while Brazil gained 2%. In the G7, Japan was by far the most successful (+10%), followed by the USA (+2%). The other five G7 members (Germany, Italy, France, the UK and Canada, in that order) notched up decreases ranging from -1% to -18%.