Supplying liquefied natural gas to the growing Asian market has become more expensive for US producers this year, a Rystad Energy report reveals. Even so, US exporters are unlikely to repeat last year’s cost-related shut-ins as global demand has rebounded to strong levels. Instead, US LNG exports climbed to a record monthly high of 6.5 million tonnes in May and may keep rising to new peaks.

Rystad Energy estimates that the short-run marginal cost (SRMC) of US LNG exports to the Asian market has risen to about $5.60 per MMBtu as of June 2021, up 65% from $3.4 per MMBtu in mid-2020 and 30% higher than last year’s average of $4.30 per MMBtu.

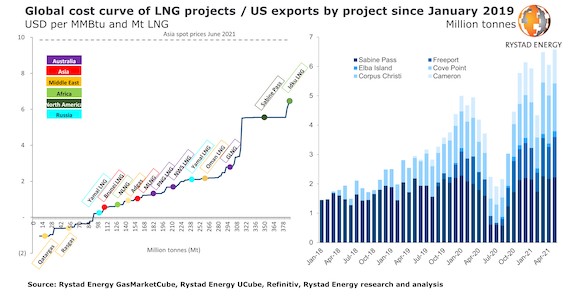

The SRMCs of currently operational liquefaction projects globally have risen this year due to a jump in transportation costs for LNG, driven by higher charter rates and fuel costs. On top of that, costs in the US have also been boosted by a recovery in domestic gas prices.

Despite the lower SRMC of LNG to Asia last year, the US was still the most expensive supplier globally. As the TTF gas prices in Europe and Asian spot LNG prices fell below $2 per MMBtu in mid-2020, US exports took the largest hit, resulting in shut-ins as buyers canceled cargoes. Rystad Energy estimates that about 12 Mt of US LNG exports were shut in last year as a result of the market crash.

“We do not see any signs of LNG shut-ins in 2021, but we do see a shift in the SRMC of global LNG and in the cost-of-supply curves. Instead, US LNG production will reach 72 Mt in 2021, its highest annual level on record, under an assumption of no shut-ins,” says Sindre Knutsson, vice president on Rystad Energy’s gas markets team.

Despite the significant cost increase, the US is not the most expensive supplier to Asia this year, however. The comeback of Egyptian LNG to the market has seen the North African country assume the role as the marginal supplier of LNG, with an SRMC of about $6.30 per MMBtu. Still, the strong demand of 2021 is expected to absorb even these costs, as Asian spot LNG prices are around $12 per MMBtu.

Meanwhile, the high transportation costs also affect producers located closer to Asia. For instance, the average cost of transporting Qatari LNG to Tokyo, Japan, has increased to $0.90 per MMBtu in 2021 from about $0.75 per MMBtu in 2020. By comparison, delivery of US LNG to Tokyo has seen an increase in voyage costs to about $1.90 per MMBtu in 2021 from $1.45 last year (already included in the US SRMC).

Some LNG projects are profitable even if prices are zero

The SRMC of liquefaction projects is not the only important price increase to influence the LNG market of late. If pre-tax liquids revenue is accounted for, many integrated LNG projects have seen improved competitiveness during 2021 thanks to higher oil prices. Pre-tax liquids revenue is calculated as the pre-tax revenue from oil activity for the upstream assets that feed LNG plants, divided by LNG production.

In that way, the variable cost of LNG can be offset by oil production revenues. For example, Qatargas 1 LNG Train 1 has an estimated variable cost of LNG production of $1.60 per MMBtu. If the pre-tax liquids revenue from the oil production is considered, the costs are offset by oil revenues of about $2.60 per MMBtu, which brings net costs down to a negative $1 per MMBtu. That way, projects like Qatargas 1 LNG Train 1 would cover their costs even if LNG prices went down to zero.

Nevertheless, there are no signs of prices falling to zero this year, or even to levels around the SRMC of Egyptian LNG at $6.30 per MMBtu. The LNG market looks robust in the short term due to the recovery in Asian and European LNG demand, supported by high demand for restocking, high CO2 prices and lower-than-expected Russian pipeline gas exports to Europe.

“Overall, the market is seeing many low-cost sources of LNG. Of the 393 Mt of LNG that we expect to be produced in 2021, over 300 Mt, or 75%, can be supplied at a cost below $3 per MMBtu, including delivery to Asia. Furthermore, 225 Mt can be delivered to the market at a price below $2 per MMBtu. This shows the diversity of the LNG market compared to other fuels, and also illustrates why LNG proved to be so robust during 2020 when Covid-19 hit the market with full force,” Knutsson concludes.