London, UK, 2nd November 2021 – Vessel operating cost inflation has slowed this year as some Covid-19 related expenses unwound and high vessel earnings encouraged some owners to postpone non-essential maintenance work, but wider macroeconomic developments are raising inflationary risks as will decarbonisation initiatives, according to the latest Ship Operating Costs Annual Review and Forecast 2021/22 report published by global shipping consultancy Drewry.

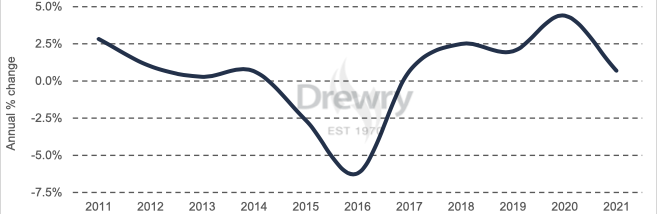

Drewry estimates that average daily operating costs across the 47 different ship types and sizes covered in the report rose 0.7% in 2021, which represented a sharp slowdown from the increase of 4.4% recorded in 2020 when opex rose at its fastest pace in over a decade. This compared to increases of 2-2.5% in the two prior years and a net 8% decline in operating costs over 2015-17 (see chart).

A high proportion of 2021 opex increases were driven by marine insurance costs which rose 4.3%, slightly higher than 4% recorded during 2020. This was due to a hardening of both hull & machinery (H&M) and protection & indemnity (P&I) premiums during 2020, and this continued into 2021. But spend declined in stores and repair & maintenance (R&M) as some Covid-19 related costs unwound and vessels had limited downtime for maintenance work during the year.

The rise in costs was broad-based across all the main cargo carrying sectors for the fourth consecutive year, albeit at a much slower rate compared with last year. The latest assessments include vessels in the container, chemical, dry bulk, oil tanker, product tanker, LNG, LPG, general cargo, reefer, roro and car carrier sectors.

Looking ahead, despite buoyant cargo demand across many vessel segments the outlook for freight markets remains highly uncertain and the prevalence of the pandemic continues to disrupt vessel operations. Hence, we expect the pressure on costs to remain which will dampen any likely inflation, but decarbonisation regulations will add to owner cost burdens over the medium term.

“Despite the mild outlook inferred by Drewry’s central opex forecast, there still exists some risk of further hardening in the insurance market as well as rising macroeconomic price inflation, both of which could inflate operating costs,” added Igbinosun. “However, we expect wider inflationary pressures to be contained by policy measures.”