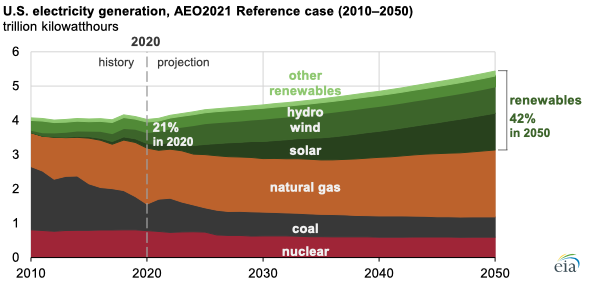

In its Annual Energy Outlook 2021 (AEO2021), the U.S. Energy Information Administration (EIA) projects that the share of renewables in the U.S. electricity generation mix will increase from 21% in 2020 to 42% in 2050. Wind and solar generation are responsible for most of that growth. The renewable share is projected to increase as nuclear and coal-fired generation decrease and the natural gas-fired generation share remains relatively constant. By 2030, renewables will collectively surpass natural gas to be the predominant source of generation in the United States. Solar electric generation (which includes photovoltaic (PV) and thermal technologies and both small-scale and utility-scale installations) will surpass wind energy by 2040 as the largest source of renewable generation in the United States.

The AEO2021 Reference case projects that the natural gas share of the U.S. electricity generation mix will remain at about one-third of total generation from 2020 to 2050. The natural gas share of generation will remain stable even though natural gas prices will remain low (at or lower than $3.50 per million British thermal units, in real dollars) for most of the projection period. This stability occurs despite significant coal and nuclear generating unit retirements resulting from market competition as regulatory and market factors induce more renewable electricity generation.

After the production tax credit (PTC) for wind phases out at the end of 2024, solar generation will account for almost 80% of the increase in renewable generation through 2050. EIA assumes that utility-scale (and commercial) solar PV facilities will receive a 30% investment tax credit (ITC) through 2023, which will then be reduced to 10% beginning in 2024 and lasts through 2050. Residential solar PV will also receive a 30% ITC through 2023, which will expire in 2024.

Because renewable energy technology costs and natural gas prices are key determinants of these projections, EIA explores sensitivity cases with varying levels of both renewable costs and natural gas price trajectories. Accordingly, the renewable technology share of generation will be higher in the Low Renewables Cost and High Oil and Gas Resource cases, relative to the Reference case, and the share of generation from renewables will be lower in the High Renewables Cost and Low Oil and Gas Resource cases.

Principal contributor: Kenneth Dubin