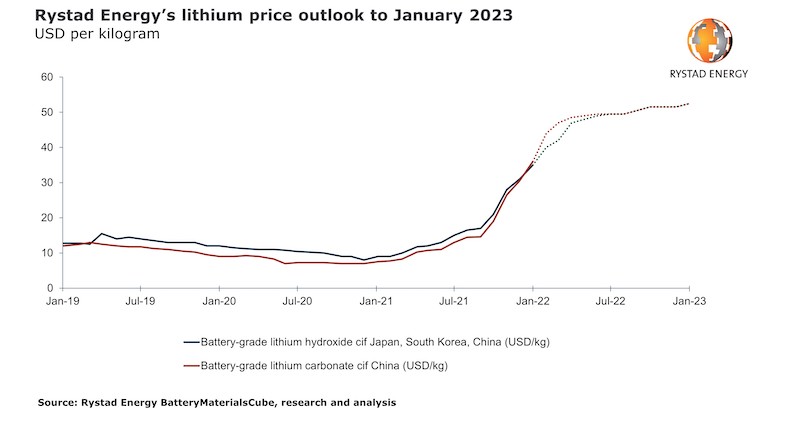

Electric vehicle (EV) producers and suppliers could be facing a major cost headache starting this year as prices for battery-grade lithium are poised to skyrocket. Prices for the metal are already trading at a record high of $35 per kilogram in Asia, and are likely to keep climbing to $50 per kilogram in the second half of 2022 and trade at around $52.5 per kilogram in January 2023, a Rystad Energy analysis shows.

Interest in lithium iron phosphate (LFP) batteries has taken off among manufacturers since early 2021. Rystad Energy therefore expects the supply of lithium salts to remain tight through the first half of 2022 at least, due to lagging production in China and South America. Producers appear reluctant to sell significant volumes on the spot market, as supply constraints and the ongoing logistical issues caused by the pandemic create bottlenecks in the trading market for lithium salts.

This supply tightness for lithium salts, combined with the optimistic demand outlook for LFP batteries that typically feed on lithium carbonate, is expected to keep lithium carbonate prices high and support a notable premium over the price for lithium hydroxide in early 2022. However, Rystad Energy estimates this premium will gradually narrow after seasonal supply bottlenecks ease in China and a ramp-up plan in South America materializes.

“A fresh new driver for China’s lithium market are lithium contract prices on the Changzhou Zhonglianjin exchange platform. Launched some six months ago, the futures contracts have driven sentiment in the market to some extent, especially over the past two months. This has contributed significantly to the current momentum in lithium prices in China and made trader-suppliers who have attempted to destock in January hold back from selling for now,” says Susan Zou, senior analyst on Rystad Energy’s battery materials team.

Changzhou’s lithium contract price for February 2022 hit an intraday high of CNY 418,500 per tonne on 10 January, up 14.34% from CNY 366,000/tonne at the close on 31 December 2021. The contract price then dropped to CNY 345,500/tonne at close on 12 January. However, it is still too early to say whether Changzhou’s lithium contract price will repeat the success of the cobalt contract on Wuxi, which has long dictated cobalt prices in China’s physical market, Zou said.

Rystad Energy’s monthly price index suggests that prices for battery-grade lithium carbonate ex-works China rose to CNY 300,000/tonne in early January 2022, up nearly 43% from CNY 210,000/tonne a month earlier. The price for battery-grade lithium hydroxide ex-works China rose to CNY 290,000/tonne in early January from CNY 192,000/tonne in early December.