On the spreads, Hong Kong trails substantially in comparison to mainland China, spreads are down to -6.02 into USA. In trans-Atlantic news, rates have been held up above $3.95 since 13th April, dropping down to $4.12 from London to US.

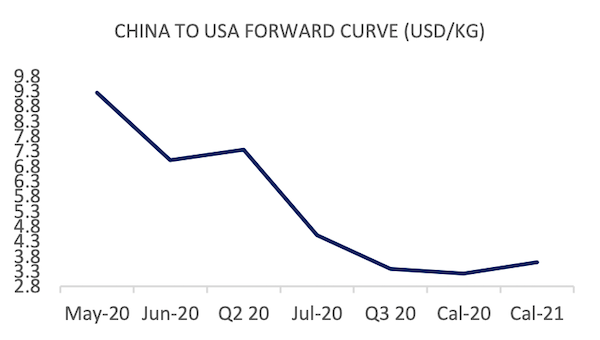

The front quarters react to the latest index prices, China to Europe lifting slightly up 37 cents on May and 32 cents for the quarter, China to USA sinks 10 cents in May, with a further 27 cents drop-off in June. The quarter is raised by indicative interest on the BID side, up to $4.50.

Market Comment

Further signs of weakness appear in the forward airfreight price, as the rates out of Hong Kong into USA completely collapse. Congestion remains in Shanghai, as cargo gets backed up across a number of the core mainland Chinese airports.

On the horizon, China locks down another City (Jilin), the 2nd this week on reports of new coronavirus cases. Meanwhile, Europe cautiously exits lockdown, for the most part, citizens are met with reports of recession (the UK GDP sunk a record 5.8%, Germany's economy shrinks 2.2%). Airlines have been rolling out post-COVID flight plans, Lufthansa is notably one of the most active in re-establishing routes (we don't know whether this is based on actual booked demand or a gamble on future demand). Certainly, cargo will take up a much bigger share of the balance sheet on these routes.

Meanwhile, the debt being piled into the travel market keeps getting bigger (often with Government strings attached), while those that can't secure life-line funds risk insolvency and bankruptcy.

So, on top of the demands of environmentalists, macro-economic turmoil (trump trade war part 2 is on the horizon), and the usual panoply of unknowns (weather, volcanoes, port strikes, oil prices), Airlines will have to tackle very high debt-loads and post-COVID travel norms in a market where one has to set up schedules based on best-possible-guesses.

On the supply side, a subtle debate circulates, is there a 'normal cargo' inventory scarcity? Where is there inventory oversupply, and which industry sectors? And how much production will move out of China in the coming months?

Volatility and uncertainty remain the only real constants for the time being.

| Basket | USD/KG | CHANGE | CHANGE % | MTD | VOL % |

| CHINA - EUR | 8.48 | 0.59 | 7.48% | 8.19 | 83.30% |

| CHINA - USA | 9.41 | -0.80 | -7.84% | 9.77 | 71.95% |

| Blended | USD/KG | CHANGE | CHANGE % | MTD | VOL % |

| PVG/EUR | 11.18 | 1.20 | 12.02% | 10.54 | 106.45% |

| HKG/EUR | 5.77 | -0.03 | -0.52% | 5.85 | 70.71% |

| PVG/US | 12.42 | 0.76 | 6.52% | 11.55 | 87.83% |

| HKG/US | 6.40 | -2.37 | -27.02% | 7.99 | 90.52% |

| Global | USD/KG | CHANGE | CHANGE % | MTD | VOL % |

| Air Index | 5.82 | -0.29 | -4.27% | 2.27 | 49.63% |

Forward Curve - Indicative Update

| FIS AFFA, CHINA - EUROPE | USD/KG | ||||

| BID | ASK | MID | CHANGE | |

| May-20 | 6.00 | 9.00 | 7.50 | 0.37 |

| Jun-20 | 4.00 | 7.55 | 5.78 | 0.00 |

| Q2 20 | 5.00 | 8.20 | 6.60 | 0.32 |

| Jul-20 | 3.00 | 5.50 | 4.25 | -0.25 |

| Q3 20 | 2.50 | 4.00 | 3.25 | -0.10 |

| Cal-20 | 2.60 | 3.50 | 3.05 | 0.00 |

| Cal-21 | 2.50 | 4.05 | 3.28 | 0.00 |

| FIS AFFA, CHINA - USA | USD/KG | ||||

| BID | ASK | MID | CHANGE | |

| May-20 | 8.00 | 10.50 | 9.25 | -0.10 |

| Jun-20 | 4.00 | 10.00 | 7.00 | -0.25 |

| Q2 20 | 4.50 | 10.20 | 7.35 | 0.50 |

| Jul-20 | 3.00 | 6.00 | 4.50 | -0.50 |

| Q3 20 | 2.50 | 4.25 | 3.38 | -0.12 |

| Cal-20 | 3.05 | 3.40 | 3.23 | 0.00 |

| Cal-21 | 3.10 | 4.10 | 3.60 | 0.00 |