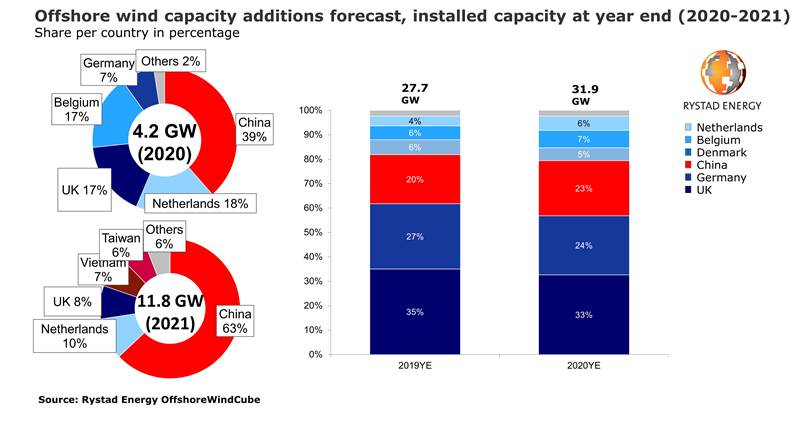

Despite the Covid-19 pandemic, the world’s installed offshore wind capacity rose by 15% in 2020, reaching 31.9 gigawatts (GW) at year-end, from 27.7 GW at the end of 2019, Rystad Energy estimates. China was the main contributor in 2020, accounting for 39% of last year’s additions, followed by the Netherlands (18%) and the UK (17%).

Rystad Energy expects the global installed offshore wind capacity to further increase by 11.8 GW in 2021, a monumental 37% step-up compared to 2020’s 31.9 GW. China will continue to lead the new capacity additions, contributing 63% of the expected growth.

However, with the first wave of the virus settling, the offshore wind market returned to a growth trajectory, supported by increased capacity targets from several nations. While staying resilient in an uncertain market was key in 2020, this year the industry finds itself positioned for record growth, especially as commissioning activities pick up pace in Asia and around the world.

After 2021, China will begin phasing out feed-in-tariffs and many developers are therefore pushing to complete projects during the coming period. As such, this year is expected to see high capacity additions in the country.

“China had a construction backlog of more than 10 GW going into 2020, and Chinese developers are racing to reach maximum commissioning by the end of the year in order to claim full feed-in-tariffs. This means 2021 is going to see major capacity additions, particularly since some projects initially scheduled for commissioning in 2020 ended up slipping into 2021,” says Alexander Fløtre, Rystad Energy’s Product Manager for Offshore Wind.

Europe and the US also saw some delays due to the pandemic. The developers of the second phase of the 50 MW Kincardine floating offshore wind project in Scotland and the Kriegers Flak combined grid solution in Denmark had to delay start-up. In the US, Danish player Ørsted announced in October delays of at least one year for five projects due to permitting issues.

Nevertheless, offshore wind developers stayed committed to their ambitions and continued to make final investment decisions for projects in 2020. The UK sanctioned more than 4.7 GW of offshore wind and the Netherlands followed with over 2.2 GW. As a result, major projects such as Triton Knoll in the UK, Borssele 3 & 4 in the Netherlands and Kriegers Flak in Denmark are expected to be completed during 2021.

In the second half of last year, almost 25 GW of capacity was added to the global backlog. Currently, Brazil has no operational offshore wind capacity, but its backlog grew significantly during 2020 as the country added more than 15 GW to the drawing board.

In addition, other regions in Asia outside China are preparing for a ground-breaking year, Taiwan and Vietnam have finally started to add significant volumes to their project pipelines – making 2021 a year to look forward to in the offshore wind market.

*Note: The report’s numbers are based on full commissioning of the wind farms to an operating level, which may diverge from grid-connected or just installed figures.