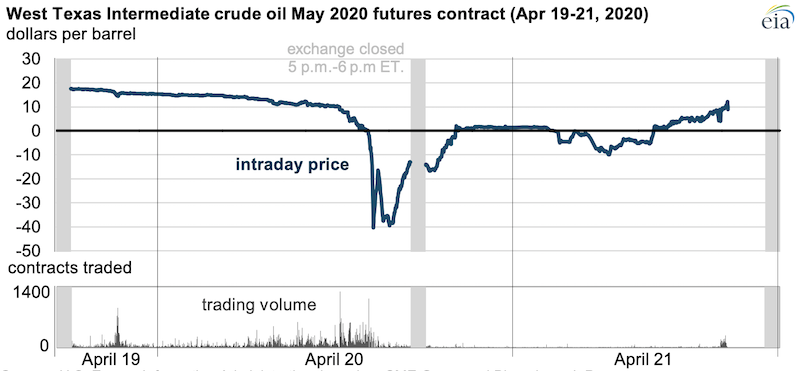

On Monday, April 20, 2020, West Texas Intermediate (WTI) crude oil front-month futures traded on the New York Mercantile Exchange (NYMEX) were priced in negative dollars per barrel (b) for the first time since trading began in 1983. At about 2:30 p.m. ET, WTI traded as low as -$40.32/b; prices remained below zero for part of the following trading day.

Market participants that hold WTI futures contracts through expiration must make or take physical delivery of WTI crude oil in Cushing, Oklahoma, unless they have made other arrangements ahead of time. Typically, most market participants close any futures contracts ahead of their expiration through cash settlement—buying or selling offsetting contracts—to avoid taking physical delivery; only about 1% of futures traded go to physical delivery. The extreme market events of April 20 and April 21 were driven by several factors, including the inability of traders who had purchased futures to find other market participants to sell futures contracts to.

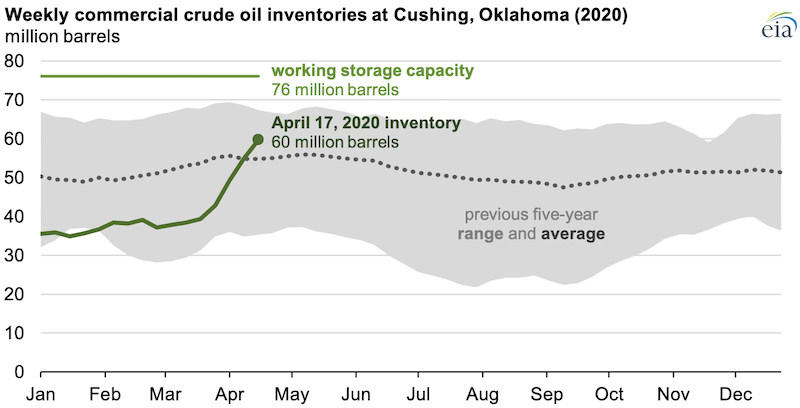

Under normal conditions, taking delivery of crude oil at Cushing purchased from the WTI futures market is straightforward. The normal physical settlement process has been affected, however, by the recent decline in the availability of uncommitted crude oil storage capacity. Consumption of crude oil and petroleum products has sharply declined following the travel restrictions and general economic slowdown in mitigation efforts for the coronavirus disease (COVID-19). As of the week ending April 17, U.S. refinery runs fell to 12.8 million barrels per day (b/d), 4.1 million b/d (24%) less than the same time last year.

As a result of this extreme demand shock, excess imported and domestically produced crude oil volumes are being placed into storage. According to U.S. Energy Information Administration (EIA) storage capacity data, crude oil storage facilities at Cushing have 76 million barrels of working storage capacity. As of April 17, Cushing inventories totaled 60 million barrels, some of which (about 2 million barrels) were in transit by pipeline, water, or rail. The remaining 58 million barrels are held in tank farms at Cushing, implying that storage was 76% full.

Although EIA data indicate that some storage remains available at Cushing, some of this physically unfilled storage may have already been leased or otherwise committed, limiting the uncommitted storage available for financial contract holders without pre-existing arrangements. In this case, these contract holders would likely have to pay much higher rates to storage operators for any uncommitted space available.

Taken together, these factors suggest that the phenomenon of negative WTI prices is mainly confined to the financial market. The positive pricing of other crude oil benchmarks (with the Brent contract for June 2020 delivery closing at $19.33/b on April 21), positive prices for longer-dated WTI prices, and positive spot prices for other (but not all) U.S. crude oils suggest that the recent price movements were predominantly driven by the timing of the May 2020 contract expiration against the backdrop of precipitous decline in consumption.

The availability of storage in Cushing will remain an issue in the coming weeks, however, and could still result in volatile price movements in the June WTI futures contract or other U.S. crude oil spot prices that face limited storage options. EIA will continue to monitor these market developments.

Principal contributors: Jesse Barnett, Jeff Barron