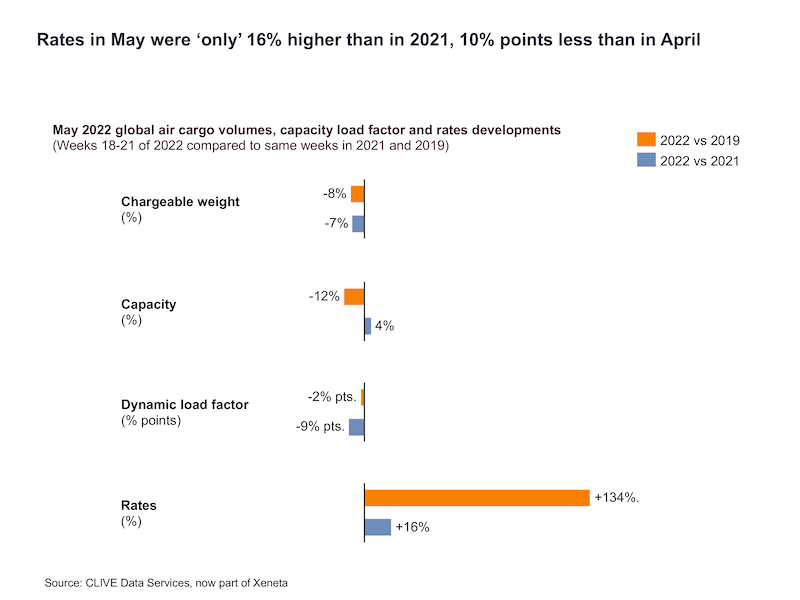

General air cargo market volumes fell -8% year-over-year in May, comparable to April, as the aviation industry’s stuttering recovery was compounded again by macroeconomic events which show no sign of abating, according to industry analysts CLIVE Data Services, part of Xeneta. The latest weekly market data also provided a glimpse of how major air cargo markets may perform in a post-Covid world.

May 2022 data shows air cargo demand -8% lower than in May 2019. Available capacity in the month of May was +4% higher versus the same month of last year but still at -12% compared to May 2019. Lower demand and increased capacity in this latest reporting period also led to a 9% pts drop in CLIVE’s ‘dynamic load factor’ last month versus May 2021, which resulted in a global load factor in May 2022 of 60%.

Air cargo market performance in May remained impacted by the continuing war in Ukraine, the ‘cost of living crisis’ causing consumers to watch their spend more carefully, stock market declines, higher interest rates, Covid-related restrictions in China, and more warnings of global recession. May’s market data showed, once again, how susceptible air cargo is to macroeconomic events, said Niall van de Wouw, founder of CLIVE and now Chief Airfreight Officer at Xeneta, the leading ocean and air freight rate benchmarking, market analytics platform and container shipping index.

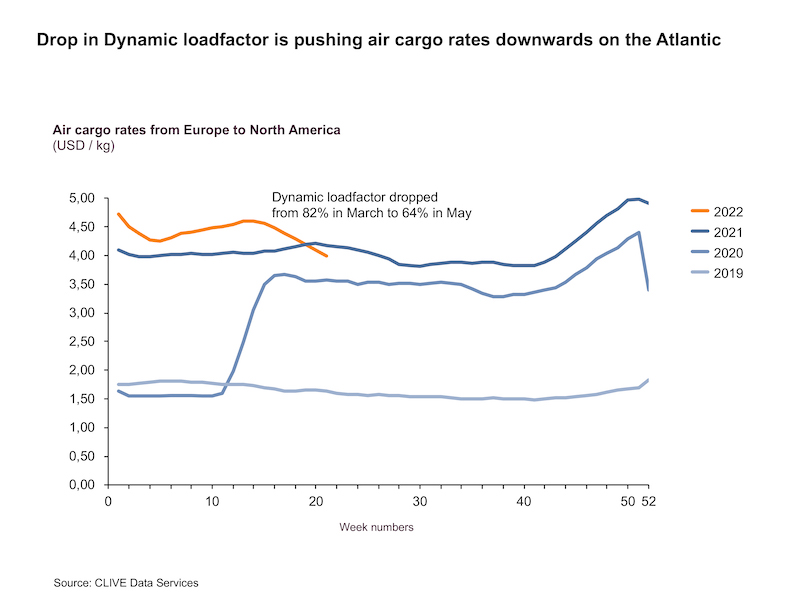

North Atlantic air cargo data in May 2022, he added, may provide a test case for the direction of other markets once they also return to their pre-Covid levels. The Europe to North America market has “changed profoundly in the last 8 weeks from load factors of 82% in March to 64% in May. May’s dynamic load factor was also 22% pts lower than in May 2021, while, in March, load factor on this lane was -7% pts lower. So, this is not just seasonality, it is the capacity coming back into this market. In March it was +44% higher than in 2021 and in May around +82%. This is a big swing, and it emphasises the jump in the cubic capacity on these routes.”

Airfreight rates have continued to drop since the return of more passenger flights and the introduction of airline’s summer schedules. In the last week of May 2022, rates from Europe to North America showed negative year-over-year growth for the first time in two years.

“The Atlantic market is interesting to follow to see how rates shift in the coming months, as it might be a bellwether on how other markets will develop when the capacity of passenger flights returns to it former level and beyond. We sense an anticipation of a slower summer market, followed by hope for growth in Q3 as is traditionally the case, but the market does not look great right now. There are more clouds on the horizon than there were two months ago,” van de Wouw said.

One light on the horizon for air cargo volumes might stem from the outcome of the current labour negotiations at US west coast ports and any potential future disruption to the ocean market across the Pacific, which he describes as “another example of an external event that has nothing to do with airfreight that could still have a profound impact on the market.”

-and-William-Lee-of-SF-Airlines-_-_127500_-_bf81080d3f4124c3d4f40d73b84e5488e09a4379_lqip.png)