The annual growth rate in the global offshore oilfield services market will likely be halved after 2022, according to Rystad Energy.

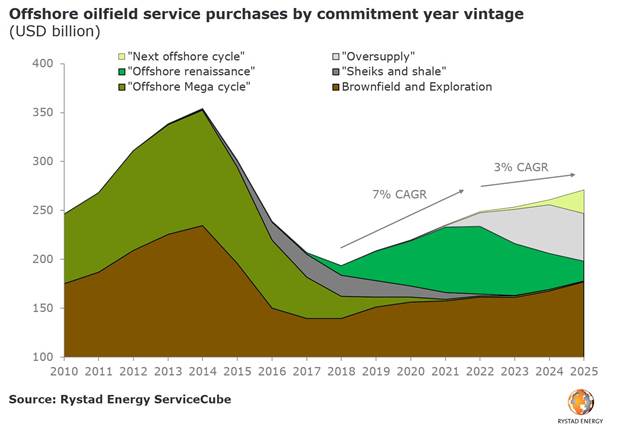

The independent energy research and consultancy headquartered in Norway with offices across the globe forecasts that the service market will slow from 7% annual growth per year in 2019-2022 to only 3% from 2022 to 2025.

He added “Higher oil prices were a primary cause of the recent upstream spending spree and – in keeping with the cyclical nature of this industry – the added production from those investments will soon help to put downward pressure on oil prices, which in turn will undermine field sanctioning activity post-2020.”

The offshore industry is currently experiencing a renaissance, with oil and gas companies ramping up their greenfield sanction activities. From 2022, however, the tide seems likely to turn, as many of the projects approved in 2018 and 2019 – representing about 5 million barrels of oil equivalent (boe) per day – will start production. In addition, four consecutive years of growth in the offshore industry will likely spur inflation in many service sectors, possibly reaching 10-15% from 2018 levels.

“The effect will be a noticeable slowdown of greenfield service purchases of platforms, subsea infrastructure, drilling rigs and vessels, causing the overall offshore service market growth rate to be cut in half,” Martinsen said.

He added “We estimate that investment commitments associated with offshore project sanctioning are likely to drop to between $70 billion and $80 billion per year – only half the amount forecast in 2020. Fewer projects sanctioned, as well as fewer completed from the ‘offshore renaissance period’ of 2018 through 2021, will likely cause the offshore service market to reach an inflection point in 2022.”

The market segments most severely affected by a slowdown will be those with a heavy exposure to greenfield activity, such as subsea equipment, offshore drilling, and SURF (subsea umbilicals, risers and flowlines). The only segment that is likely to see an increase is engineering.