Russia’s industrial-metal exports are sinking as the country’s invasion of Ukraine prompts commodity buyers and financiers to pull back from its powerhouse producers, according to executives and analysts tracking trade flows.

The nation’s top steelmakers have seen exports drop since the incursion began, while nickel shipments have also been affected, people with knowledge of the matter said. While the response to Russia’s actions differs from country to country, Germany has halted almost all steel purchases, one of the people said, asking not to be named given the commercially sensitive nature of the transactions.

Russia’s metal shipments are falling and buyers are “hesitant in the context of sanction uncertainty and escalation,” Goldman Sachs Group Inc. analysts said in a note. “With materially reduced export volume out of Russia, Kazakhstan and Uzbekistan, all the base-metal markets will face accelerated tightening in the near-term,” they said, without specifying how they’re tracking trade flows.

Some shippers are refusing to transport Russian commodities such as nickel, but the impact on volumes so far has been minor, another person familiar with the matter said. MMC Norilsk Nickel PJSC is Russia’s only producer of nickel.

Prices rose on the London Metal Exchange Monday, with nickel adding as much as 3% and aluminum jumping as much as 5% to a fresh record of $3,525 a ton.

“Our operations are proceeding as usual, we continue to meet all our contractual obligations and remain committed to our clients and partners,” a spokesperson for Nornickel said.

Banks were already limiting their exposure to Russian shipments before this weekend’s further round of sanctions, which exclude some Russian banks from the SWIFT messaging system and also penalize the country’s central bank. At least two of China’s largest state-owned lenders are restricting financing for purchases of Russian commodities, underscoring the limits of Beijing’s pledge to maintain economic ties with one of its most important strategic partners.

In Europe, Societe Generale SA and Credit Suisse Group AG stopped financing commodities trading from Russia, people familiar with the matter said. The two banks, key financiers to commodity trading houses, are no longer providing funds to move raw materials such as metals and oil from the country.

Russia’s invasion has roiled markets worldwide from energy to grains, heaping more inflationary pressure on a global economy already grappling with soaring costs. U.S. officials are said to be weighing exemptions for transactions involving the energy sector in a bid to tame surging oil prices. But if similar dispensations were granted for metals, it’s unlikely that flows would return to normal quickly, given the turmoil in Black Sea freight markets, Goldman said.

Rusal Halt

Russia’s United Co. Rusal International PJSC, the world’s top aluminum producer outside China, came under further strain on Monday as it halted shipments at an alumina refinery in Ukraine that feeds its smelters at home.

Aluminum traded up 0.6% at $3,376.50 a ton as of 5:25 p.m. in London.

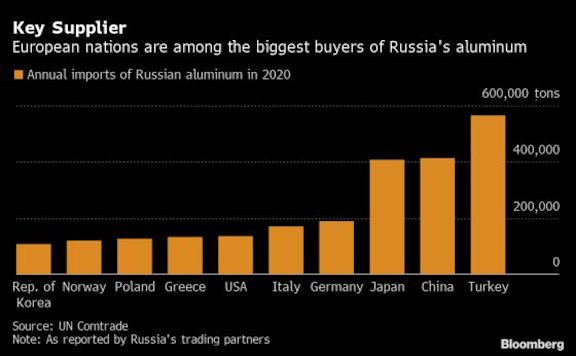

Turkey was the single largest buyer of Russian aluminum in 2020, ahead of China, Japan and Germany, according to UN Comtrade data. Italy and Greece are also major importers.

“As a result of sanctions, should counterparties be unable to transact with UC Rusal as was the case in 2018, then there is a risk that all of UC Rusal’s overseas alumina assets could be impacted,” Ami Shivkar, principal analyst in Wood Mackenzie’s aluminium team, said in a note. “Any significant reduction in alumina production would impact primary metal output in short order leading to even greater primary aluminum market deficits.”

While Russia’s commodities trade is facing immediate threats, the country’s producers also fear longer-term risks arising from sanctions targeting its imports of high-tech products. Russia’s mining companies are reliant on equipment and software licenses from overseas vendors, executives at three of the firms said.