Snapshot of crude and product freight rates, supply-demand

posted by AJOT | Apr 12 2024 at 08:57 AM

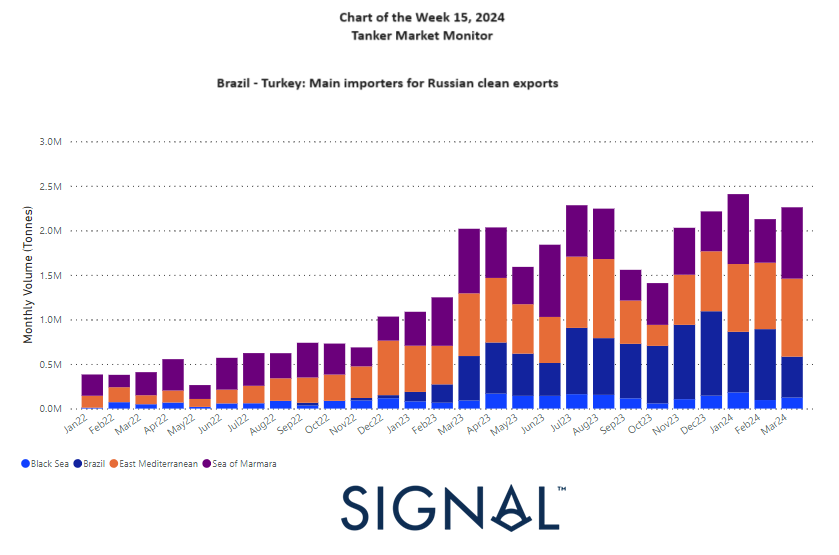

Chart of the Week: The main importers of Russian clean exports from 2023 onwards, Brazil and Turkey emerged as primary importers of Russian clean exports

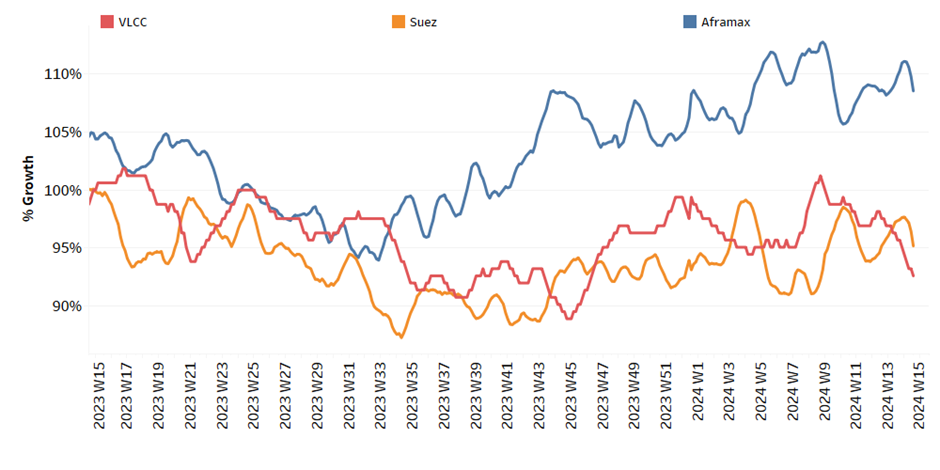

In the second week of April, the crude oil freight market maintained a relatively stable sentiment in the VLCC Ras Tanura segment, while indications of an upward trend emerged in the Aframax Mediterranean, accompanied by a decrease in vessel supply. April appears poised to challenge the sentiment in the VLCC freight market, as there are signals of increased vessel activity for Ras Tanura, despite the tonne-day demand growth slowing down, with the last peak observed almost seven weeks ago.In the clean segment, it's noteworthy to observe the growth of Russian clean oil exports to Brazil and Turkey, which have emerged as the primary destinations since last year. Meanwhile, US crude oil prices have intriguingly displayed signs of pulling back to $85/bbl, with market concerns about inflation pushing back expectations for Fed rate cuts to later in the year. At present, worries about inflation seem to have overshadowed concerns about a potential Iranian strike on Israel.

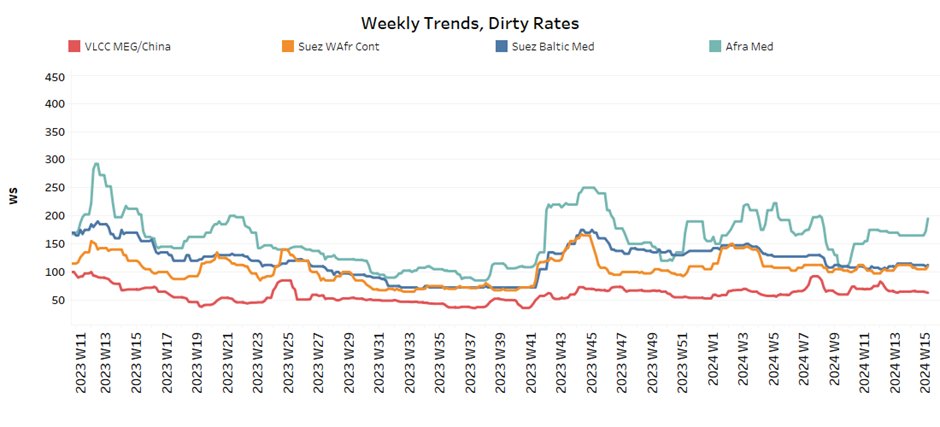

Towards the end of the second week of April, sentiment on the crude oil freight market was remarkably stable in the VLCC and Suezmax vessel segments. In the Aframax-Med segment, however, there were signs of an upward shift in sentiment.

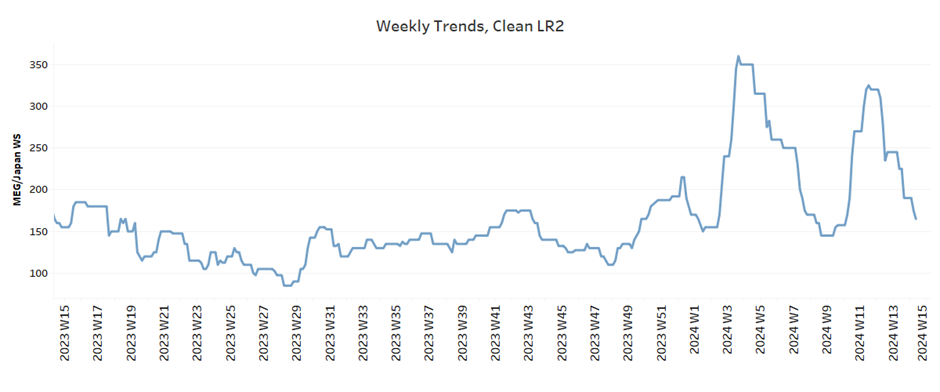

The VLCC MEG-China freight rates held steady at 63WS, marking a 10% monthly decline from the peak observed in mid-February at WS90. The prevailing indication suggests that April will likely persist with a softening trend. However, the question remains whether rates will rebound to WS70 by month-end.

Suezmax freight rates for shipments originating from West Africa to continental Europe have maintained a level slightly above 120WS, indicating a 4% annual increase. In the Suez Baltic Med route, rates appeared to reflect a firmer momentum, standing at 128WS, but marked a 25% decrease compared to the previous year.

Aframax Med freight rates surged by 200 WS, showcasing a significant 30% monthly upturn. Despite this robust increase, current rates remain marginally 5% lower compared to the same period last year.

‘Product’ WSLR2 Weaker

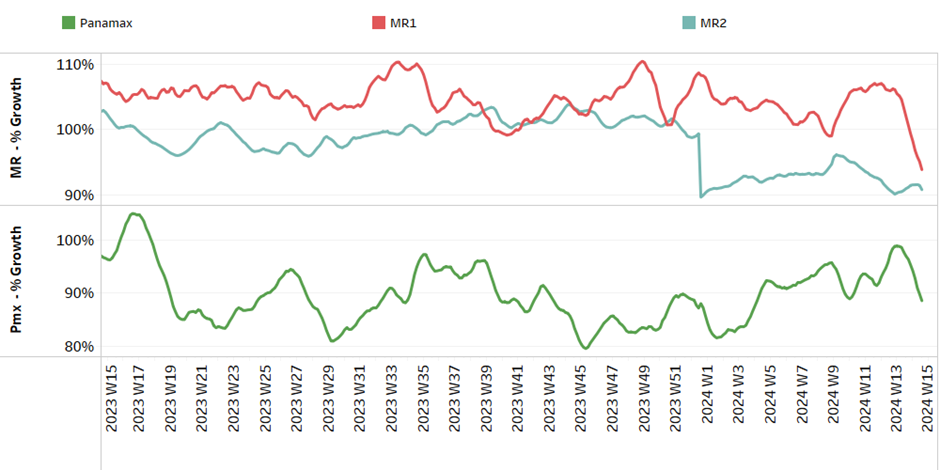

LR2 AG freight rates sustained their downward momentum, dipping below the 170WS threshold. This signifies a notable 27% decrease compared to the prior week, with rates currently standing 5% lower than during a comparable week a year ago.

LR1 Weaker

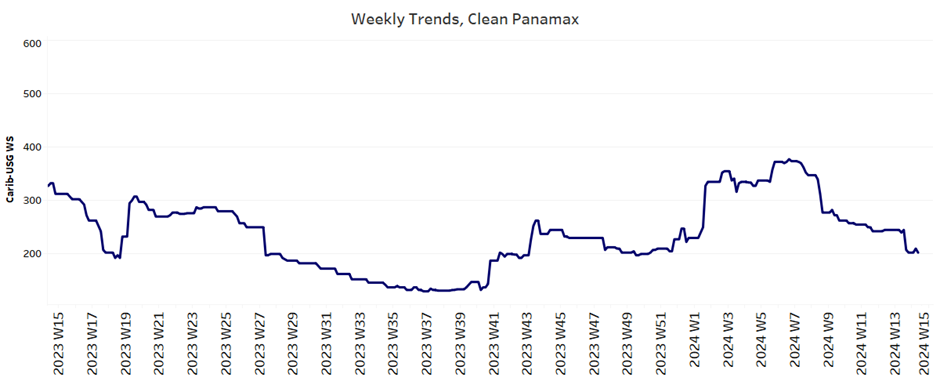

Panamax Carib-to-USG rates have declined to 205WS, marking a 37% decrease compared to the rates observed during a comparable week a year ago.

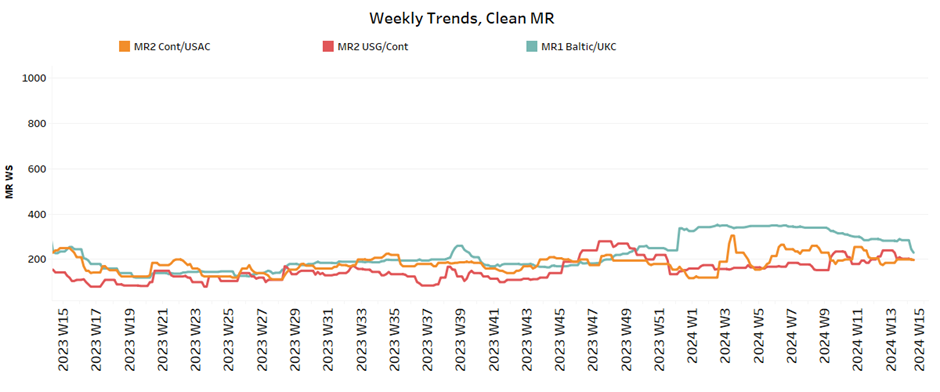

‘Clean’ MR Weaker

MR1 rates for shipments from the Baltic continent have shown a weakening trend, hovering around 230WS. Today's sentiment reflects a decrease of 27% from the rates observed a month ago. Meanwhile, MR2 rates for shipments from the continent to the USAC have plummeted to 180WS, marking an 8% decrease compared to rates observed a month ago.

SECTION 2/ SUPPLY

‘Dirty’ (# vessels) - Mixed

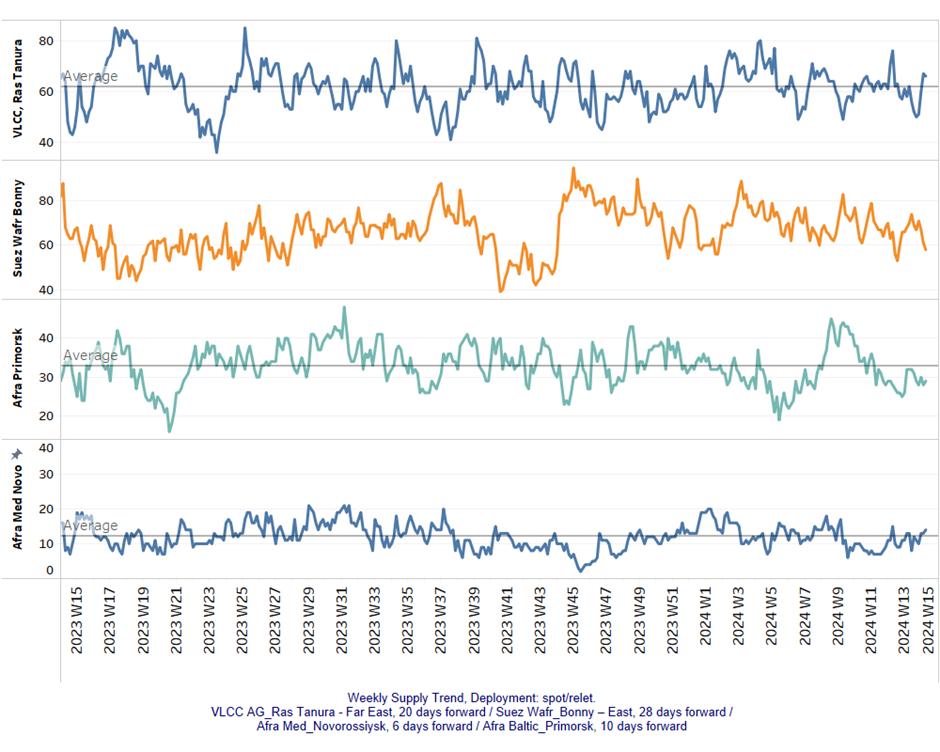

The supply trend for crude tankers is showing an upward trajectory in the VLCC Ras Tanura and Aframax Med segments, while a downward trend appears to persist for the Suez Wafr Bonny and Aframax Primosk segments.

VLCC Ras Tanura: The ship count has exceeded the annual average of 60, with indications of an upward revision for the next few days in April compared to the lows recorded in the previous two weeks.

Suezmax Wafr: The current number of ships has fallen below 60, a remarkable drop of 13 from the previous week, while the downward trend has continued over the last two weeks.

Aframax Primorsk: The current ship count sustained levels below the annual average of 30 for the last two weeks, representing a nearly 38% decrease from the peak recorded during week

Aframax Med Novo: The vessel count has begun to trend above the annual average of 10, but there's noticeable volatility at the start of April.

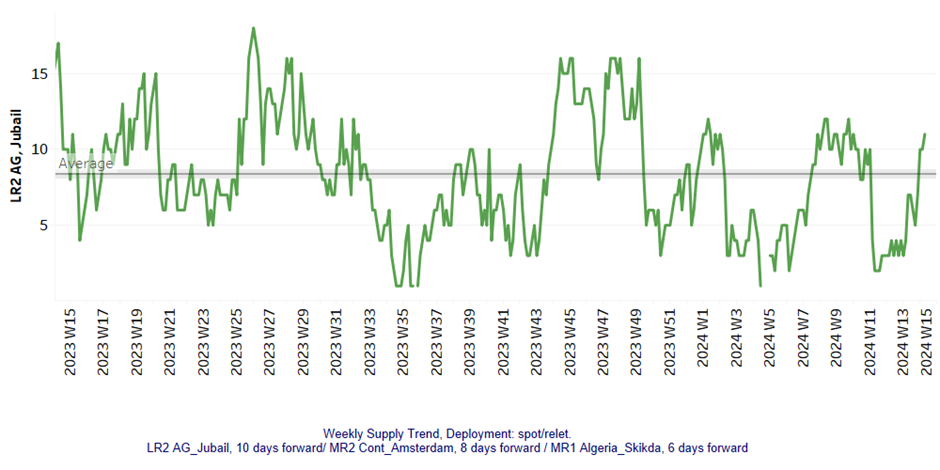

'Clean' LR2 (#vessels) - Increasing

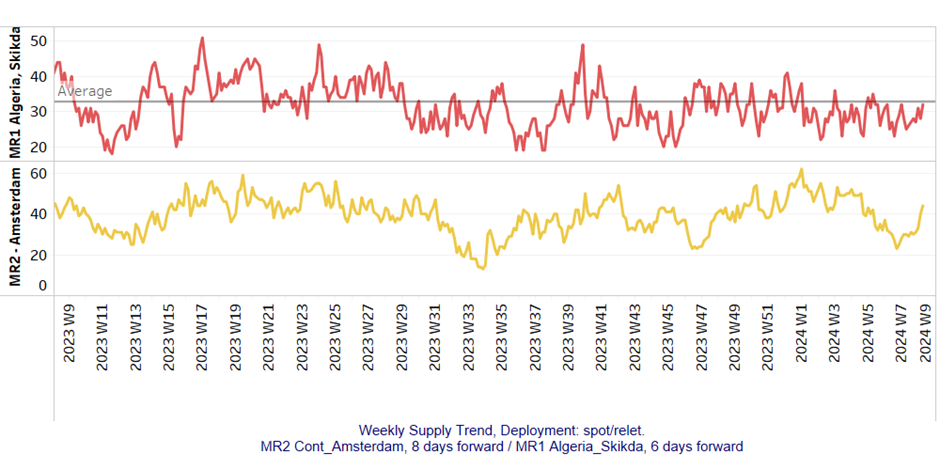

MR (#vessels) - Decreasing

Clean LR2 AG Jubail: The upward trend has been notably revised, with recent levels now hovering above the annual average of 10 and rising to similar highs observed in week 9.

Clean MR: Vessel activity for MR1 in Algeria's Skikda port has stayed below the annual average since the end of week 13, with around 24 vessels recorded. Similarly, in MR2 Amsterdam, there has been a decline to 28 vessels, significantly lower than the peak of around 50 observed during week 11.

SECTION 3/ DEMAND (Tonne Days)

‘Dirty’ Decreasing

Dirty tonne days: Over the past two weeks, the growth trajectory in the VLCC segment has fallen behind that of Suezmax vessels, marking a downward trend towards the end of the month. Meanwhile, in the Aframax segment, the increase in dirty tonne days appears to have decelerated since the beginning of April, although it remains elevated compared to the low point observed before the end of January.

‘Clean’ Decreasing

Panamax tonne days: The second week of April contradicted earlier weekly estimates, which had hinted at a potential upward trend revision. Instead, recent lows matched the growth levels recorded during week 11.

Clean MR tonne days: Over the past six weeks, tonne-day growth for both MR1 and MR2 vessel sizes has consistently been on a downward trajectory. Specifically, in the MR2 category, the growth remains notably subdued, marking its weakest performance since the start of the year.