Strong increase ex-Asia boosts global air cargo tonnages and rates

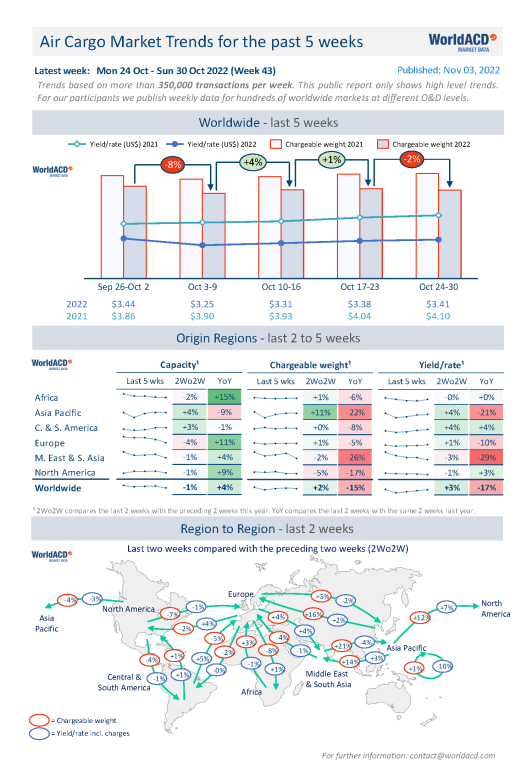

A strong recovery in volumes from Asia Pacific to Europe and North America in the last two weeks of October has helped lift overall global volumes and average rates back into positive territory following months of gradual declines and a sharp dip in the first half of October, the latest preliminary figures from WorldACD Market Data reveal.

Comparing weeks 42 and 43 with the preceding two weeks (2Wo2W), tonnages were +2% above their level in weeks 40 and 41, while average worldwide rates were up

+3%, in an almost flat capacity environment – based on the more than 350,000 weekly transactions covered by WorldACD’s data.

Across that two-week period, outbound volumes from Asia Pacific rose by +11% compared with the previous two weeks. On a lane-by-lane basis, strong increases were recorded from Asia Pacific to, respectively, Europe (+16%), Middle East & South Asia (+14%), and North America (+12%). Meanwhile, tonnages from North America dropped -5%, falling -7% to Europe and -4% to Asia Pacific.

Elsewhere across that two-week period, Europe to Africa recorded the biggest drop in tonnages, declining -8%, the same as reported last week. The strongest increase in tonnages was from the Middle East & South Asia to Asia Pacific (+21%), on a 2Wo2W basis.

Asia market strengthening

On the pricing side, average rates are globally on a slight upward trend, driven by origin regions Asia Pacific and Central & South America (both +4%) and Europe (+1%), while outbound rates from the Middle East & South Asia have shown a continuously negative trend for the last 5 weeks. On a lane-by-lane basis, rates from Asia Pacific to North America showed the most notable increase (+7%), but there was a steep drop in intra-Asia Pacific average prices (-10%), on a 2Wo2W basis.

The double-digit volume increases ex-Asia Pacific towards the end of last month may hint at some strengthening of that market in the normally seasonally strong fourth quarter (Q4) of the year, although it may be more of a bounce-back from China’s Golden Week holiday in the first week of October, plus the reopening of some markets – including Hong Kong – following recent Covid restrictions. With only a modest corresponding uplift in rates, it still seems unlikely to be a sign of a significant Q4 peak season, and certainly nothing like the scale seen last winter.

Year-on-Year perspective

Comparing the overall global market with this time last year, chargeable weight in weeks 42 and 43 was down -15% compared with the equivalent period in 2021, despite a capacity increase of +4%. Notably, tonnages ex-Asia Pacific are -22% below their strong levels this time last year, and the Middle East & South Asia origin tonnages are -26% below last year.

Capacity from all the main origin regions, with the exception of Asia Pacific (-9%) and Central & South America (-1%), is significantly above its levels this time last year, including double-digit percentage rises from Africa (+15%) and Europe (+11%), and a +9% increase from North America.

Worldwide rates are currently -17% below their levels this time last year at an average of US$3.41 per kilo, despite the effects of higher fuel surcharges, but they remain significantly above pre-Covid levels.